This article was written and first appeared on Fundflicks – Warner Bros Discovery (fundflicks.net)

If you have not familiarized yourself with Warner Bros. Discovery Inc. (Nasdaq: WBD), maybe you might be interested to find out more after reading this article.

Subscription videos on demand and streaming have been prevalent over the last decade and consumers have a plethora of choices to choose from these days, from the likes of Netflix (currently the largest streaming company in the world by market cap) to Disney Plus and Warner Bros Discovery.

Competition is intense but it is good for the consumers and the markets.

These companies are increasingly focus on refining and streamlining their operations, including providing more choices for consumers at a fraction of what they used to pay.

Last year, the spin-off merger between AT&T’s Warner Media unit and Discovery created quite a bit of a buzz – the combined company, Warner Bros. Discovery, Inc. has since started refining operations of their own.

Warner Bros Discovery’s portfolio includes the likes of Discovery Channel, Warner Bros. Entertainment, CNN, HBO, HBO Max, Cartoon Network, and franchises like “Batman” and “Harry Potter”.

A top priority for David Zaslav, CEO who is a long-time veteran in the industry is to make streaming video as profitable as the old TV business.

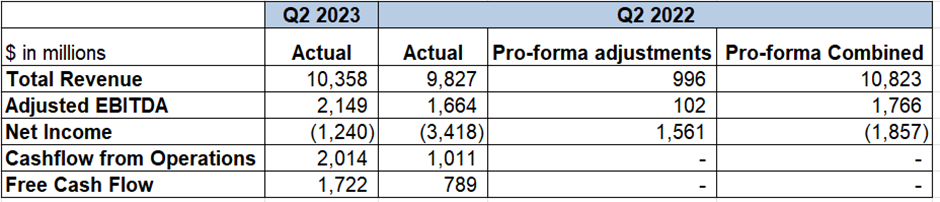

Financial Highlights for Q2 2023

Warner Bros. Discovery, Inc. (Nasdaq: WBD) has recently reported earnings for the second quarter ending 30 June 2023.

A quick summary of the financial highlights is appended below:

- Total revenues for Q2 came up to $10,358 million.

- Total adjusted EBITDA for Q2 was profitable at $2,149 million.

- However, the Group incurred a net loss of -$1,240 million as it included a $1,658 million of pre-tax amortization from the earlier acquisition of related intangible assets and $146 million of pre-tax restructuring from the merger.

- Cash flow from operating activities increased to $2,014 million in this quarter.

- Free Cash Flow for this quarter amounted to $1,722 million.

- Debt prepayment of $1.6 billion in this quarter. The company has $47.8 billion of gross debt and $3.1 billion of cash equivalents. Net gearing leverage is at 4.6x.

Source: Brian 3F Compilation

For clarifications, pro-forma combined results represent the combined results of the Company and the WarnerMedia business.

Studio Segment:

The studio segment can be said to be cyclical in nature due to the timing of the production.

For instance, tv revenue was down in this quarter as compared to the previous year due to the fewer CW series timing of production held this year. Consequently, games revenue also declined because last year included the release of mega gaming events such as LEGO Star Wars. A popular franchise series such as Batman – was also scheduled for last year release.

Overall, this resulted in lower revenues and adjusted EBITDA overall for the studio segment this quarter as compared to the last year same period.

Networks Segment:

For the networks segment, distribution revenue did better this quarter primarily driven by the increase in US contractual affiliate rates.

The advertising revenue, however, has declined in this quarter as the absence of NCAA March Madness Championship broadcasts negatively impacted the results. The unit broadcasted the NHL Stanley Cup Finals this year which mitigated the situation.

Overall, revenues were lower at $5,758 million in this segment as compared to the pro-forma combined last year of $6,121 million.

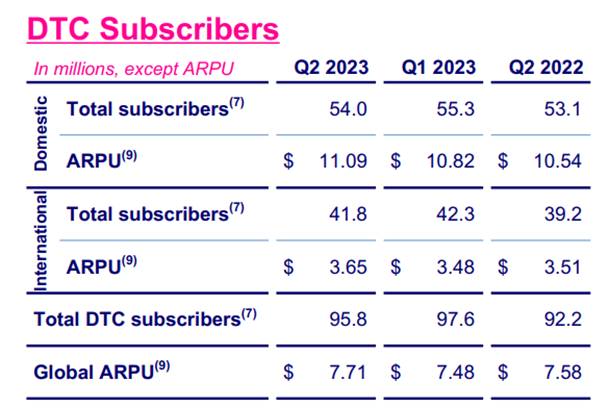

Direct-to-Consumer (D2C) Segment:

For the D2C segment, revenues were 14% higher than the pro-forma combined numbers at $2,732 million vs $2,410 million.

These were driven primarily by content revenues which grew significantly due to the timing of library licensing deals.

Subscribers’ growth in this quarter also led to the higher advertising revenue in this segment.

Total DTC subscribers grew in this year for both domestic and international to 95.8 million, as compared to 92.2 million last year in the same period.

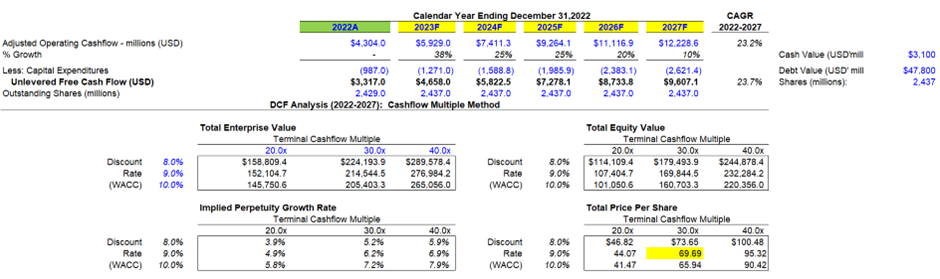

Valuation Model: Discounted Cash Flow Analysis

The company generated $3.3b worth of free cash flow for 2022 and management has guided for 2023 free cash flow to be in the range of $4.6b-$5b. For the purpose of conservative, I have used the lower half of the range in my model.

This is a highly insane cash flow generative model, and we are only at the start of the monetization and growth.

Investors have been shunning this company because of its huge debt profile which the company managed to voluntarily repay off $7b back in 2022, and a further $1.6b in 1H 2023. The debt currently stands at $47.8b with a gearing level of 4.6x.

Management has guided to target gearing level to comfortably be below 4.0x by end 2023 and 2.5x-3.0x by end 2024. With such a huge generative cashflow, they will be able to bring it down in a matter of time.

Under this model, we assume the current enterprise value that takes into account the $3.1b cash equivalents and $47.8b debt value in the book. We then applied a good sub-growth of 38% increase (which management has guided) in 2023 further by a 25% increase in the next two years. Growth will then drop down to 20% by 2026 and then 10% from thereon in 2027 onwards.

At a terminal cashflow multiple of base range of 30x (Netflix is trading at EBIT level of 44x), this stock is worth close to $70/share. This won’t be prominent and apparent to investors yet because the company is still busy repaying down debt but when debt gearing has gone down to reasonable level, we can expect share price to fly from here.

My target value is this should be worth close to $70/share, which at current price of ~$11represents more than 6x return.

Look out for Warner Bros Discovery, they are one worth to watch out.