Lululemon has caught the attention of many value investors lately, as it has fallen almost half from the start of this year (since hitting the peak in Dec last year) due to the slower growth and weak spending consumption, impacting many other consumer discretionary and luxury stocks particularly this year.

With the stock currently trading at the ~$250 range as of writing, can we see this an opportunity to purchase a quality business at a reasonable valuation? Is this an appealing opportunity for investors to initiate a position in this stock? Let us dig in more to find out.

Business Overview

Lululemon Athletica, is a Canadian athletic apparel retailer known for its high-quality yoga pants, leggings, and other athletic wear. Founded in 1998 by Chip Wilson in Vancouver, Canada, Lululemon initially focused on yoga wear before expanding its product line to include a variety of athletic and casual clothing, as well as accessories for men and women.

Lululemon is renowned for its high-quality, durable fabrics and innovative designs, which cater to both performance and comfort.

The company promotes a healthy and active lifestyle, often integrating mindfulness and wellness into its brand ethos.

From a community and retail branding point of view, Lululemon frequently hosts free yoga classes and other fitness-related events in its stores and local communities, fostering a sense of community and loyalty among its customers.

Since its founding, Lululemon has grown significantly, with stores across North America, Europe, Asia, and Oceania. The company continues to expand its product range and global presence.

Known for its excellent customer service, Lululemon emphasizes creating a personalized and engaging shopping experience both in-store and online.

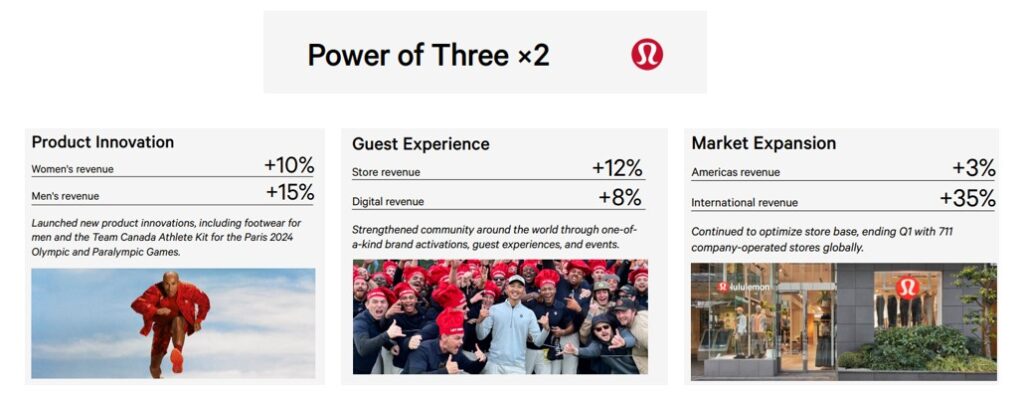

Power of Three 2x Strategy

The “Power of Three x2” strategy refers to Lululemon’s ambitious growth plan initially laid out by CEO Calvin McDonald. This strategy focuses on three key areas for driving growth, with an aim to double the company’s revenue. The primary components of this plan consist of:

Product Innovation: Lululemon aims to continually innovate its product lines. This includes expanding the range of offerings in both men’s and women’s apparel, as well as exploring new categories such as self-care and footwear. The focus is on leveraging advanced fabrics and design technology to meet the evolving needs of customers.

Guest Experience: Enhancing the customer experience is central to this strategy. Lululemon plans to deepen its relationship with customers through personalized services, in-store experiences, and digital engagement. Initiatives like community events, fitness classes, and a robust online shopping experience are part of this focus.

Market Expansion: Lululemon seeks to grow its global footprint by expanding into new markets, especially in regions like Asia and Europe. The strategy includes opening new stores and increasing brand awareness through localized marketing efforts.

The “x2” aspect refers to the company’s goal of doubling its revenue, building on the success of the initial “Power of Three” strategy. By doubling down on these core areas, Lululemon aims to significantly increase its market share and achieve sustained growth.

We can see that in the first quarter of its recently announced results last month, the company has done relatively well on the three aspects of their strategies, all delivering positive results.

International markets, especially the China Mainland market, contributed 14% of the total net revenue for the company, and has increased 45% year on year. The Rest of the World contributed 13% of the total net revenue, and has increased 27% year on year.

They have executed the China market very well, especially considering that Nike’s apparel impact from Greater China only contributed a 10% increase year on year, while footwear only increases by a mere 2%.

The North America contribution is the massive worry though, as it has only grown by 3% year on year, and this region contributed the highest margins out of all the markets they are operating.

Overall, gross margins were almost flat at 57.7% of net revenue, versus 57.5% of net revenue the previous year.

Lululemon has also been trying hard to pivot their business towards launching more products for the male population, but it is one which I am just not convinced enough that it will move the needle for them, especially when there are heavy competition out there in sports apparel for male dominated.

Valuation

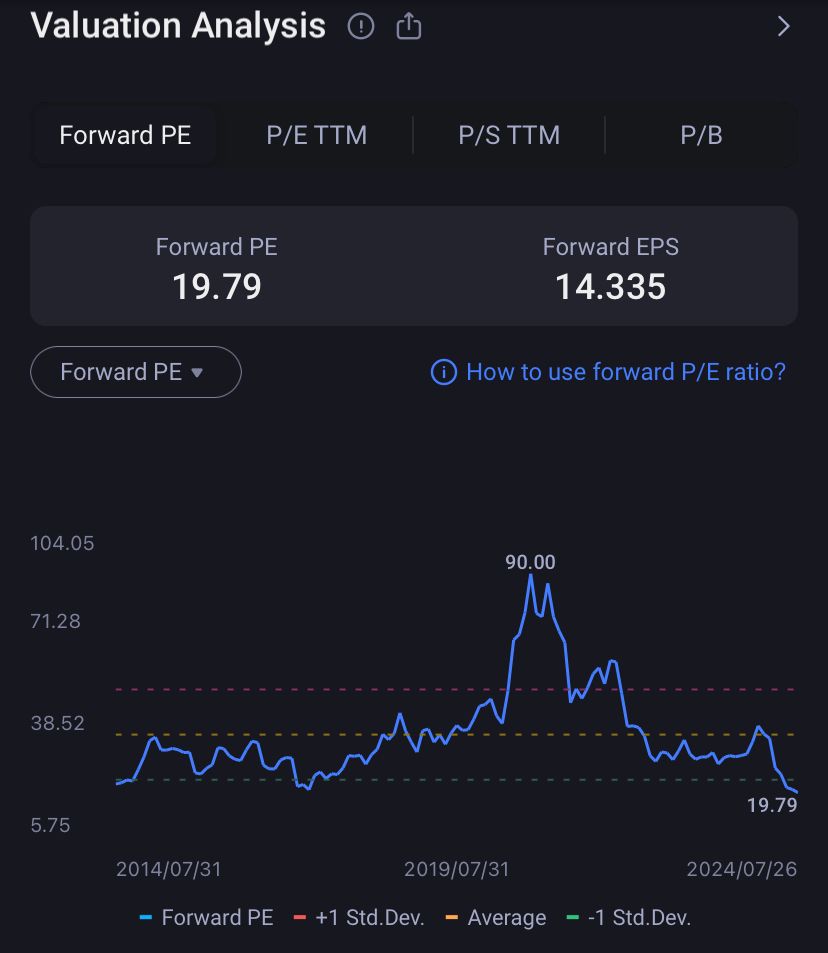

Today’s share price is equivalent to its share price back then during the peak right before Covid hits back in Feb 2020, but it’s worth to note that its Earnings Per Share (EPS) has grown ~3x from then till now, which objectively speaking comparatively it does look cheap at the moment.

Currently, Lulu trades at a trailing Price to Sales of 3.7x, a trailing Price to Earnings of 23x, and a forward Price to Earnings of 19.7x. Comparatively speaking, Lulu has never traded at such a cheap valuation based on historical perspective.

The million dollar in question is about how much Lulu can successfully execute their “Power of three 2x” strategy and how fast they can move to grow their presence in market share.

There will be headwinds from a slower consumption and increasing competition that might derail their plans like any other business.

While Lulu has guided for a 11-12% projection growth for next year, boosted by the +35 to 40 net new company-operated stores projections in 2024, this is much slower than the growth the company used to grow at in the past.

The problem with valuation multiple is when the growth slows down, the valuation multiple gets downgraded as well, so you get a double whammy from a slower EPS growth plus the lower multiples. The same goes on the other direction where the company starts registering higher growth, and higher multiples will apply.

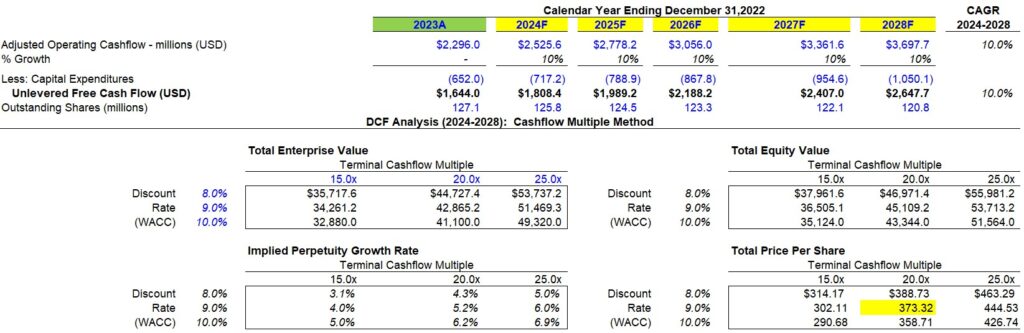

We run a DCF projection based on a conservative 10% growth rate from today all the way through 2028.

The $1 billion share buyback program approved by the board will help reduce the company’s outstanding shares and increase its EPS over time.

At the 20x multiple, the company’s intrinsic value is worth $373, which is close to a 50% margin of safety from the current share price of about $253.

Even if we had applied a lower multiple of 15x, the company’s intrinsic value is still worth $302, which is still a decent 20% margin of safety away from the current share price.

Because the company is trading at such a depressed valuation at the moment, I think there may be opportunities for value investors to come in for those interested in this space.

The biggest risk remains however whether Lulu can sustain and grow its brand name and become a major powerhouse like Nike one day.

Follow me, if you have not, on my social media channel here!